From 1 November 2025, the Support at Home Program replaced the Home Care Package Program, introducing new ways to deliver and manage home care services. At the same time, the New Aged Care Act brings significant reforms to residential aged care delivery and management.

For more information please refer to our Support at Home Hub and Residential Aged Care Hub.

Aged care fees and charges change on 20 March and 20 September each year.

Here is a summary of the Schedule of Fees and Charges for Residential and Home Care as of 20 March 2026.

How Much Does Aged Care Cost in Australia?

Home and residential aged care contributions depend on how much income and assets an individual has. Costs change regularly due to indexation against the Age Pension and CPI. Fees are indexed on 20 March and 20 September each year.

What If I Can’t Afford Aged Care?

In Australia, the aged care system is set up so that everyone can access quality care regardless of their financial situation. There may not be as broad a choice of facilities for people with fewer assets, but there are always options, and contributions can be deducted directly from pension payments.

Find out more about what happens if you can’t afford aged care.

See answers to 7 frequently asked questions about aged care fees.

Fees and Charges for Support At Home

Support at Home replaced the four-level Home Care Packages program from 1 November 2025. There is no basic daily fee under Support at Home. Instead, participants contribute a percentage of the cost of each service they receive, based on the service type and their income and assets

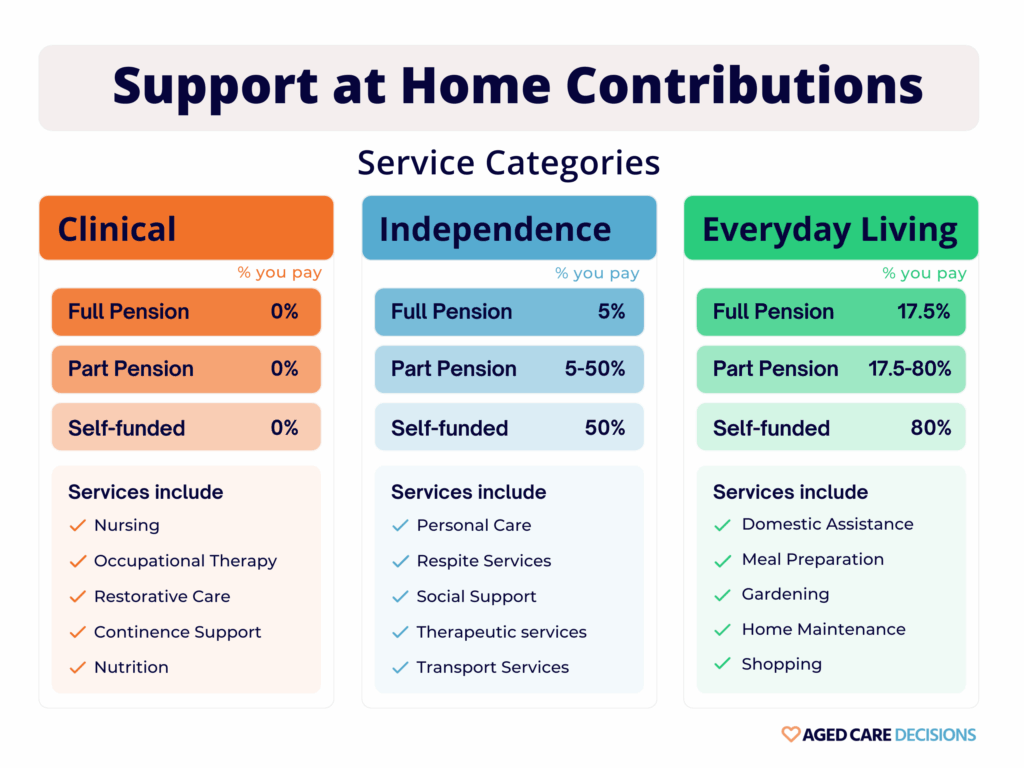

Support at Home Service Categories & Contributions

All Support at Home services fall into one of three categories, each with different contribution rates.

How Is Your Contribution Rate Determined?

Services Australia conducts an income and assets assessment (also called a means assessment) to determine your contribution rates. Your pension status is the main factor. Full Age Pensioners pay the lowest rates, while self-funded retirees pay the maximum. You can still access Support at Home without an assessment, but you may be charged at the maximum rate.

For people who are not on the Age Pension, contribution rates for Independence and Everyday Living services are also affected by non-pension income. The thresholds below show where income testing begins to affect contribution rates.

Non-Pension Income Threshold | Single | Couple (combined) | Couple, Illness Separated (combined) |

Minimum threshold (contributions begin) | $5,668 | $9,880 | $9,880 |

Maximum threshold (full contribution rate applies) | $101,105 | $161,768 | $202,210 |

Between the minimum and maximum thresholds, contributions are calculated on a sliding scale. Above the maximum threshold, the full contribution rate for your category applies.

Read our simplified guide to income and means assessments in aged care.

Lifetime Cap For Support at Home

Once you reach the lifetime cap, you will no longer be asked to pay contributions for non-clinical services, regardless of how long you continue to receive Support at Home.

Cap Type | Amount |

New participants (from 1 Nov 2025) | $137,917.01 |

Grandfathered HCP participants (approved before 12 September 2024) | $86,185.23 |

Lifetime caps are indexed on 20 March and 20 September each year.

Note: Any contributions you paid under an old Home Care Package or under Support at Home count towards the combined residential aged care lifetime cap.

The “No Worse Off” Principle (Grandfathered Home Care Package Recipients)

If you were approved for, or were receiving, a Home Care Package on or before 12 September 2024, you are protected by the “no worse off” principle:

- If you did not pay fees under your Home Care Package, you will never pay contributions under Support at Home, even if you are later assessed at a higher classification.

- If you did pay fees, your contributions under Support at Home will be the same or lower than what you paid previously.

Find out about the “no worse off” principle.

Support At Home Classification Budgets

Your Support at Home classification determines the maximum government budget available to fund your care each quarter. Provider prices and administration costs are drawn from this budget. You pay your contribution percentage on top of what the government subsidises.

| Classification | Quarterly Budget | Annual Budget | Typical Care Level |

| 1 | $2,683 | $10,732 | Minimal support — light housework, welfare check-ins |

| 2 | $4,008 | $16,035 | Light personal care, medications, social activities |

| 3 | $5,491 | $21,966 | Moderate support — regular personal care, meal prep, cleaning |

| 4 | $7,424 | $29,696 | High-frequency support — daily routines, continence care |

| 5 | $9,924 | $39,697 | Daily support and health coordination |

| 6 | $12,028 | $48,113 | Comprehensive care — nursing, wound care, allied health |

| 7 | $14,536 | $58,147 | Intensive daily care — complex health, dementia support |

| 8 | $19,526 | $78,106 | Highest level — palliative, specialised equipment, nursing |

Budget amounts are subject to indexation and Government amendment. Accurate as at November 2025.

Find out what you can spend your Support at Home budget on.

Service and Management Fees

Support at Home providers cannot charge separate package management or administration fees. All provider costs (including administration, coordination and travel) must be included in the all-inclusive service price. This means your contribution is simply your percentage of the total service price.

Read our guide to Support at Home service agreements and how provider pricing works.

Financial Hardship Assistance for Support At Home

If you cannot afford your assessed contributions after covering essential living costs (housing, food, utilities, medical), you may be eligible to apply for financial hardship assistance through Services Australia.

For more information on how to apply see our 8-step guide to applying for financial hardship support under Support at Home.

Transition Care Program

Transition care helps older people get back on their feet after a hospital stay. It provides short-term care for up to 12 weeks, including social work, nursing support, personal care, and allied health care.

State and territory governments are the approved providers of transition care. The aged care schedule of fees relating to this is outlined below.

| Maximum Daily Fee | Rate |

| Transition care delivered in a home or community setting | $13.75 |

| Transition care delivered in residential aged care | $66.80 |

Find Support At Home Providers In Your Area

Aged Care Decisions offers a FREE and independent service to help you find and compare Support at Home providers that suit your care needs and budget. We also provide valuable support and advice for all stages of your aged care journey.

Residential Aged Care Fees and Charges

In Australia, residential aged care fees and charges are broken down into three areas: the Basic Daily Fee, Care Contributions (means tested), and Accommodation Fees.

Read our guide to nursing home costs in Australia.

Basic Daily Care Fee

This covers basic living costs such as food, laundry, cleaning and power. The basic daily fee is not means tested. Everyone entering residential aged care pays it.

The basic daily fee is set at 85% of the single basic Age Pension and is indexed on 20 March and 20 September each year.

| Maximum Basic Daily Fee | Rate |

| Residential aged care | $66.80 |

| Additional costs for residents in designated remote areas | An additional $1.06 per day may apply |

At $66.80 per day, the basic daily fee equates to approximately $24,382 per year. This fee can be transferred directly from your pension.

Care Contributions (Means Tested)

From 1 November 2025, how much you contribute to your care costs in residential aged care depends on which fee arrangement applies to you.

Means Tested Care Fee (1 July 2014 to 31 October 2025 Fee Arrangements)

Residents who entered care between 1 July 2014 and 31 October 2025 pay a means tested care fee in addition to the basic daily fee. This fee is calculated based on income and assets, including the resident’s home if they own one.

The means tested care fee is calculated based on:

- Marital status

- Home ownership status and who is living in the home (e.g. a partner, carer or close relative)

- Annual income

- Total financial assets including superannuation

- Debts or loans

Means tested fees are determined by a means assessment coordinated by Services Australia or the Department of Veterans’ Affairs.

Means Tested Care Fee Caps

The maximum amount any individual will pay towards means tested care fees is:

| Means Tested Care Fee Caps | Rate |

| Annual cap | $35,910.43 |

| Lifetime cap | $86,185.23 |

Both caps are indexed on 20 March and 20 September each year.

Non-Clinical Care Contribution and Hotelling Contribution (1 November 2025 Fee Arrangements)

Residents entering permanent residential aged care from 1 November 2025 are on new fee arrangements with two separate contributions replacing the means tested care fee.

| Contribution | Maximum Daily Rate |

| Hotelling contribution (covers hotel-style daily living costs) | $22.15 per day |

| Non-clinical care contribution (contributes to personal and nursing care) | $107.32 per day |

Services Australia advises the exact amount each resident is asked to pay based on their means assessment.

Non-Clinical Care Contribution Caps:

| Non-Clinical Care Contribution Cap | Amount |

| Daily cap | $107.32 |

| Four-year time-limited cap | The fee ceases after a cumulative total of 4 years (1,460 days) of paying the non-clinical care contribution, even if the lifetime cap has not yet been reached |

| Lifetime cap | $137,917.01 |

Both the daily cap and lifetime cap are indexed on 20 March and 20 September each year. The four-year time-limited cap is measured in days, not dollars, and is therefore not indexed.

Contributions paid under Support at Home or previous home care income-tested fees count toward the lifetime dollar cap, but not toward the 4-year time-limited cap.

Residential Care Means Test —Income and Asset Thresholds

The table below outlines how much income an individual can earn per year before they must contribute means tested fees for residential aged care.

| Income Free Area For: | Rate |

| Single person | $35,313.20 |

| Couple, illness separated (single rate) | $34,585.20 |

| Couple, living together (single rate) | $27,310.40 |

If an individual earns less than these amounts, their income is excluded from the income component of the residential aged care means test. This means they will only pay the basic daily care fee.

After income exceeds the lowest threshold, there are stages of income that determine how much you are asked to contribute:

Income threshold | Rate | Rate |

Income free area | $35,313.20 | $34,585.20 |

First income threshold | $87,947.60 | $87,219.60 |

Second income threshold | $101,105.00 | $101,105.00 |

Third income threshold | $117,230.20 | $117,230.20 |

Fourth income threshold | $141,252.80 | $138,340.80 |

Residential Care Means Test — Asset Thresholds and Home Exemption Cap

Asset threshold | Rate |

Asset free area | $64,500.00 |

First asset threshold | $214,884.00 |

Second asset threshold | $258,000.00 |

Third asset threshold | $361,366.66 |

Fourth asset threshold | $536,384.00 |

Home exemption cap (per person) — the net value of the home above this amount is excluded from the value of the resident’s assets. | $214,884.00 |

Use the My Aged Care fee estimator to work out how much you will pay in means tested fees for residential aged care.

Accommodation Fees

The cost of a room in a residential aged care facility can be paid via a Refundable Accommodation Deposit (RAD), a Daily Accommodation Payment (DAP), or a combination of both.

Refundable Accommodation Deposit (RAD)

The average RAD in Australia is about $470,000, but prices vary greatly depending on location and facility type. The RAD is often an advertised price and is negotiated between the resident and the aged care facility.

Not everyone pays a RAD to enter residential aged care, as this payment is means tested against income and assets.

A resident with annual income over $86,185.23 and more than $214,884.00 in assets will generally be asked to pay the full RAD.

If a resident has income below $35,313.20 and assets below $64,500, the Australian Government will pay the accommodation costs.

The maximum RAD that can be charged without prior pricing authority approval is $758,627.

Daily Accommodation Payment (DAP)

If your income and assets are above the threshold for government support, but you cannot, or do not want to pay a Refundable Accommodation Deposit (RAD) upfront, you can choose to pay a Daily Accommodation Payment (DAP) instead. The DAP covers the cost of your room on an ongoing basis (usually paid fortnightly or monthly) and is not refundable.

The DAP is calculated by multiplying the room’s RAD by the Maximum Permissible Interest Rate (MPIR) set by the Australian Government, and dividing by 365 days.

As of 1 April 2026, the MPIR is 7.96%. For example, the Daily Accommodation Payment for a room with a RAD of $500,000 would be:

$500,000 × 7.96% ÷ 365 = $109.04 per day

The DAP is based on the MPIR applicable on the day the accommodation price is agreed. It does not change with future movements in the MPIR unless you move to a different facility or enter into a new accommodation agreement.

From 1 November 2025, for residents entering under the new accommodation arrangements, DAPs are also indexed twice yearly (on 20 March and 20 September) in line with CPI. This means that while the MPIR component remains fixed, the payable DAP may increase over time due to indexation.

You can choose to pay for your room using a combination of a RAD and DAP.

Thresholds For Refundable Deposits and Daily Payments

| Threshold | Rate |

| Minimum asset level after paying RAD (assets protected) | $63,000 |

| Maximum RAD without pricing authority approval | $758,627 |

Two Examples of How Residential Aged Care Fees and Charges Are Calculated

Meet Bill.

Bill is a widower in his nineties. He is less mobile than he used to be, and after discussions with his family, he has decided to move into a residential aged care facility.

Bill paid off the home he lives in many years ago and owns an investment property outright. This property generates an income of $35,400 per year. Bill has $75,000 in the bank and $125,000 in superannuation. The market value of his home is $1,350,000.

Based on a means test, Bill will pay the basic daily care fee and a means-tested care fee (subject to annual and lifetime caps). He will also pay an accommodation payment, which can be structured as a RAD (lump sum), a DAP (daily payment), or a combination of both.

Bill may decide to sell his home and pay for his accommodation as a RAD. Alternatively, he could retain or rent out the property and use the income to help pay a DAP. The way his former home is treated under the aged care means test may affect the fees he pays.

Meet Angela.

Angela is 87 and needs full-time care. She has no superannuation, very little cash outside of her pension, and does not own property.

Based on her means test, Angela will likely only need to pay the basic daily care fee (which is typically deducted from her pension). As she has low income and minimal assets, the Government will subsidise most of the cost of her care and may also pay an accommodation supplement to the provider on her behalf. Depending on her assessment, she may pay no accommodation costs or a small contribution.

Her choice of rooms or providers may be more limited depending on availability and pricing, but she will still have access to appropriate care.

At Aged Care Decisions we assist you at every stage of your aged care journey.

Our 100% FREE aged care matching service helps over 10,000 Australian families each month.

We use custom-built software that takes your location, budget, specific care needs and personal preferences, and creates a tailored aged care Options Report for you. This report narrows your search down to only include vacancies and available providers that match your needs.

Watch the video below for an explanation of how our service works: